Managing personal finances can be overwhelming, especially when balancing daily expenses, long-term goals, and financial literacy in an increasingly complex economic landscape.

For many individuals, gaining control over their finances means navigating a maze of expenses, savings, and unexpected costs—often without the right tools or guidance.

This project started as a result of my personal frustration with trying to understand my own expenses, leading to a guilt that shaped my money-spending decisions that affected my personal and social well-being.

The Challenge

How can I help individuals take control of their finances by making smarter budgeting and saving decisions that align with their financial goals?

THE HIGH-LEVEL GOALS THAT DEFINED MY DESIGN

Make financial management simple and time-efficient

Encourage healthy financial habits through actionable steps

The Solution

Learning better financial habits with Cashly

Cashly is a platform that makes taking control of your finances simple. Through intuitive budgeting tools, helpful learning materials, and personalized insights, users gain the confidence to manage their money effectively and work toward their financial goals.

Intuitive Budgeting and Goal Setting

Based on research conducted with individuals facing various financial challenges, Cashly enables users to set personalized budgets and savings goals tailored to their financial priorities—whether that’s building an emergency fund, paying off debt, or saving for a big purchase. With reminders and progress tracking, Cashly helps users stay on course, encouraging consistency and long-term financial habits.

Helpful Learning

89% of survey respondents stated they don’t consider themselves financially literate. To address this, Cashly offers engaging short articles and videos that simplify complex financial concepts. Users can save learning materials directly to their financial journal, allowing them to revisit key insights as they build their financial knowledge at their own pace. This approach empowers users to make informed decisions and gain confidence in managing their money.

Personalized Insights

Cashly offers personalized financial insights, including notifications about changes in your spending or progress toward goals. You’ll get alerts if you're spending more in a category or need to update your contributions. The AI chatbot lets you ask questions or explore financial scenarios, with insights easily saved to your financial journal for future reference.

Don't want to link your card or use AI?

39% of survey respondents expressed concern about AI accessing their finances. To address this, access to the AI is optional—you have full control over whether or not you choose to use it. Additionally, you can manually input your expenses and opt out of adding a card if you prefer.

Bridging the gap between financial uncertainty and financial confidence

Financial decisions can feel overwhelming, and without the right guidance, it's easy to feel stuck or discouraged. As life gets busier, it becomes increasingly harder to manage your money.

By providing learning material and personalized budgeting tools with actionable steps to help users take control…

and implementing personalized insights and reminders for them to draw upon…

Cashly empowers you to make smarter financial decisions with ease.

Research

White Paper Research

Before designing Cashly, I conducted quick white paper research to better understand the scope of financial instability so I could begin to think where a UX-driven solution could make an impact.

I found in my research that In 2023, around 35% of households with incomes below $50,000 a year are living paycheck to paycheck, struggling to maintain savings while navigating rising living costs and unexpected expenses. The National Financial Educators Council describes financial instability as a vicious cycle:

"Where money problems cause stress, leading to mental health struggles, which then make it even harder to earn, manage finances, or seek help, ultimately deepening financial hardship."

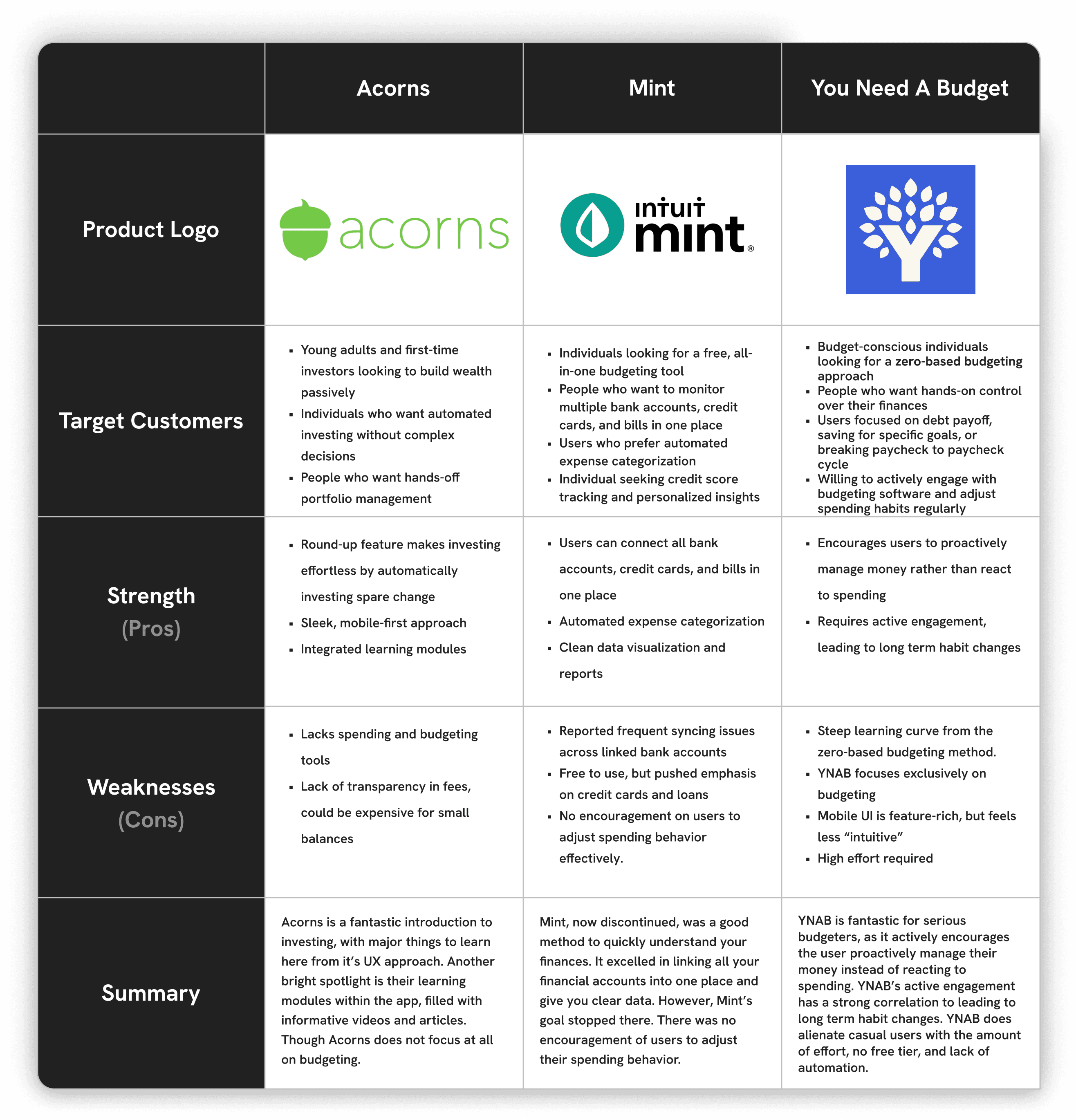

Competitor Analysis

My white paper research confirmed that my feelings of financial anxiety were not unique. This research led me to ask:

What are others doing to help people take control of their finances?

I looked at and analyzed three competing platforms: Acorns, Mint, and You Need A Budget.

After my initial analysis of the competitors, I could make the assumption that Cashly could further help the user take control of their finances in three key areas:

Take a holistic approach to financial planning

All of these competitors focus on different areas of money management. Acorns focuses on investing, YNAB for budgeting, and Mint for tracking. Users could benefit from a platform that connects the dots between the different areas of money management.

Combine financial education with actionable steps

Acorns provides valuable learning modules, but its automated investing approach limits users from actively applying their knowledge. As a result, users may gain financial insights without developing strong, hands-on money management habits.

Focus on ease of use and time

Acorns and Mint prioritize ease of use but lack robust budgeting tools. Acorns focuses on automated investing, while Mint struggled with syncing issues and failed to encourage proactive management. Cashly can bridge this gap by combining automation with real-time budgeting tools, helping users stay in control without added complexity.

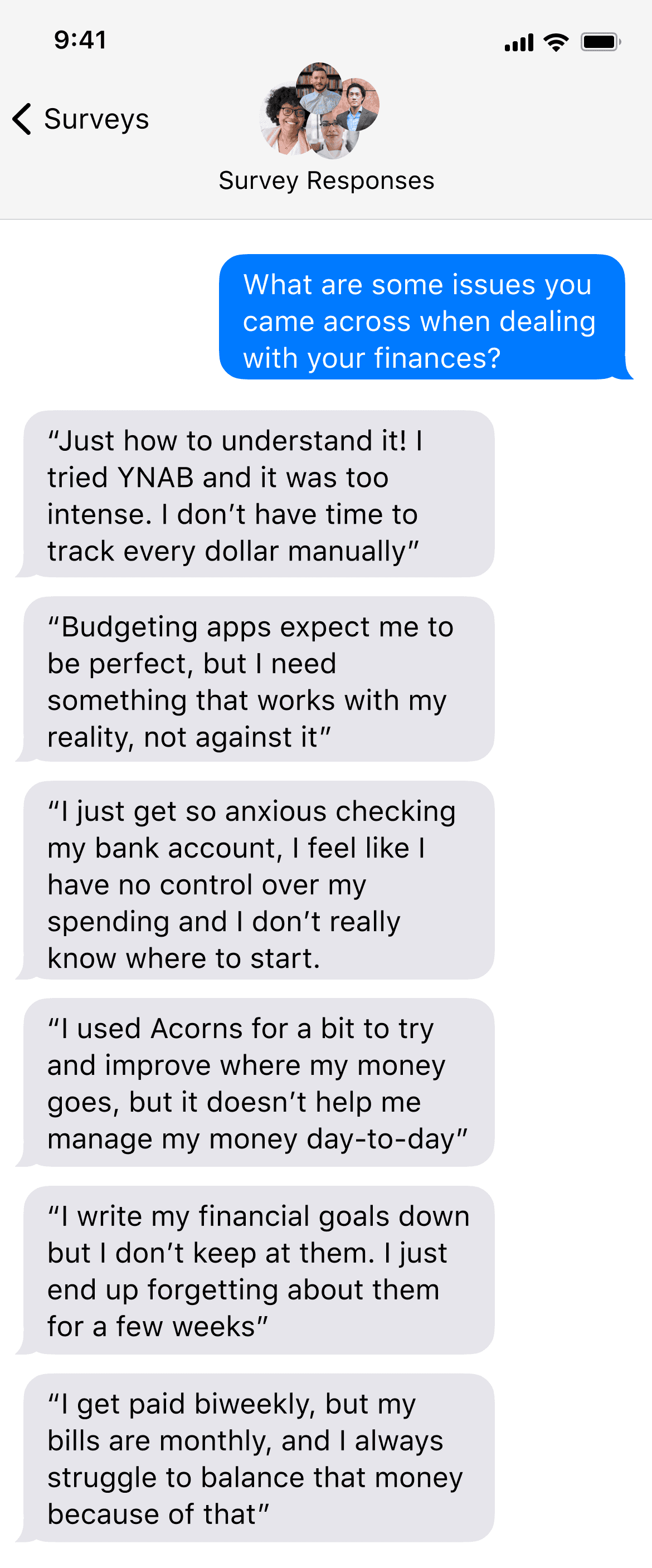

Validating Assumptions Through Survey Respondents

Continuing forward with my research, I sent out a survey to understand and begin to hear about people's relationships with their finances.

36 survey respondents shared their difficulties with managing their finances.

Unique responses recorded that highlighted a specific problem with managing finances, or experience using competitor's platforms

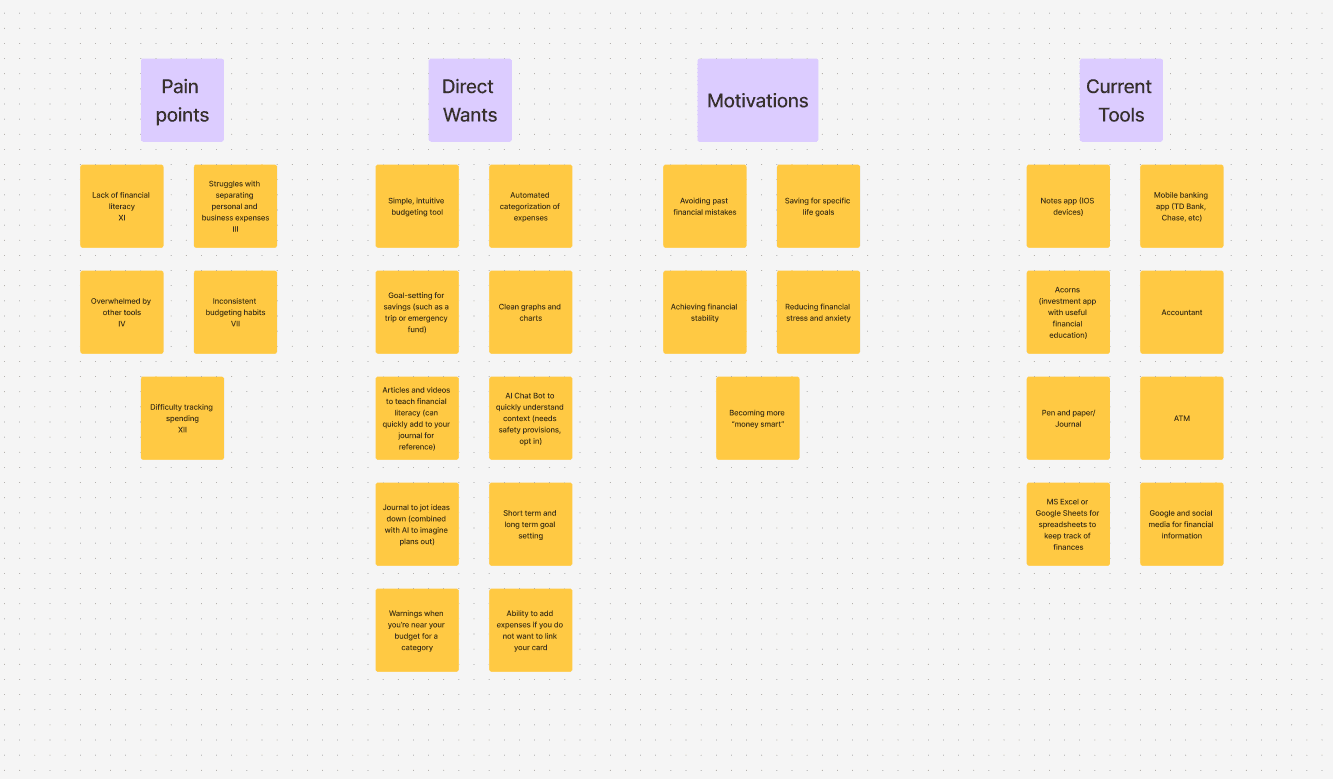

Survey questions revolved around four core aspects that would be used to organize the user research through affinity mapping: Pain Points, Direct Wants, Motivation, and Current Tools.

Of the 36 survey respondents, I conducted in-depth interviews with 14 to better understand their financial management experiences. I then organized their insights into an affinity diagram, serving as a key reference point for feature development and design decisions.

Pain points were given roman numerals to identify how many of the interviewees had a specific pain point they ran into.

Key Insights from Research

Users struggle with:

Fragmented financial tool usage

Limited financial literacy

Emotional barriers

Users rely on multiple apps (Acorns for investing, Mint for tracking expenses, YNAB for budgeting) to manage different aspects of their finances. This fragmentation creates friction, as no single tool effectively consolidates all their needs in one place.

Many users experience stress, anxiety, and avoidance when it comes to managing their finances. The fear of seeing low balances, difficulty maintaining financial habits, and feeling like budgeting tools demand perfection contribute to disengagement.

Users struggle with basic financial concepts, such as balancing income with expenses and setting sustainable financial goals. Existing tools assume a level of knowledge users don’t always have, and few provide educational resources to help them develop healthy money habits.

From all of this research, I came to the conclusion that:

Financial management is fragmented, overwhelming, and inaccessible—users juggle multiple tools, struggle with anxiety around money, and lack the guidance needed to build lasting financial habits.

This led to me implementing two high-level objectives that guided my design of Cashly

Make financial management simple and time-efficient

Encourage healthy financial habits through actionable steps

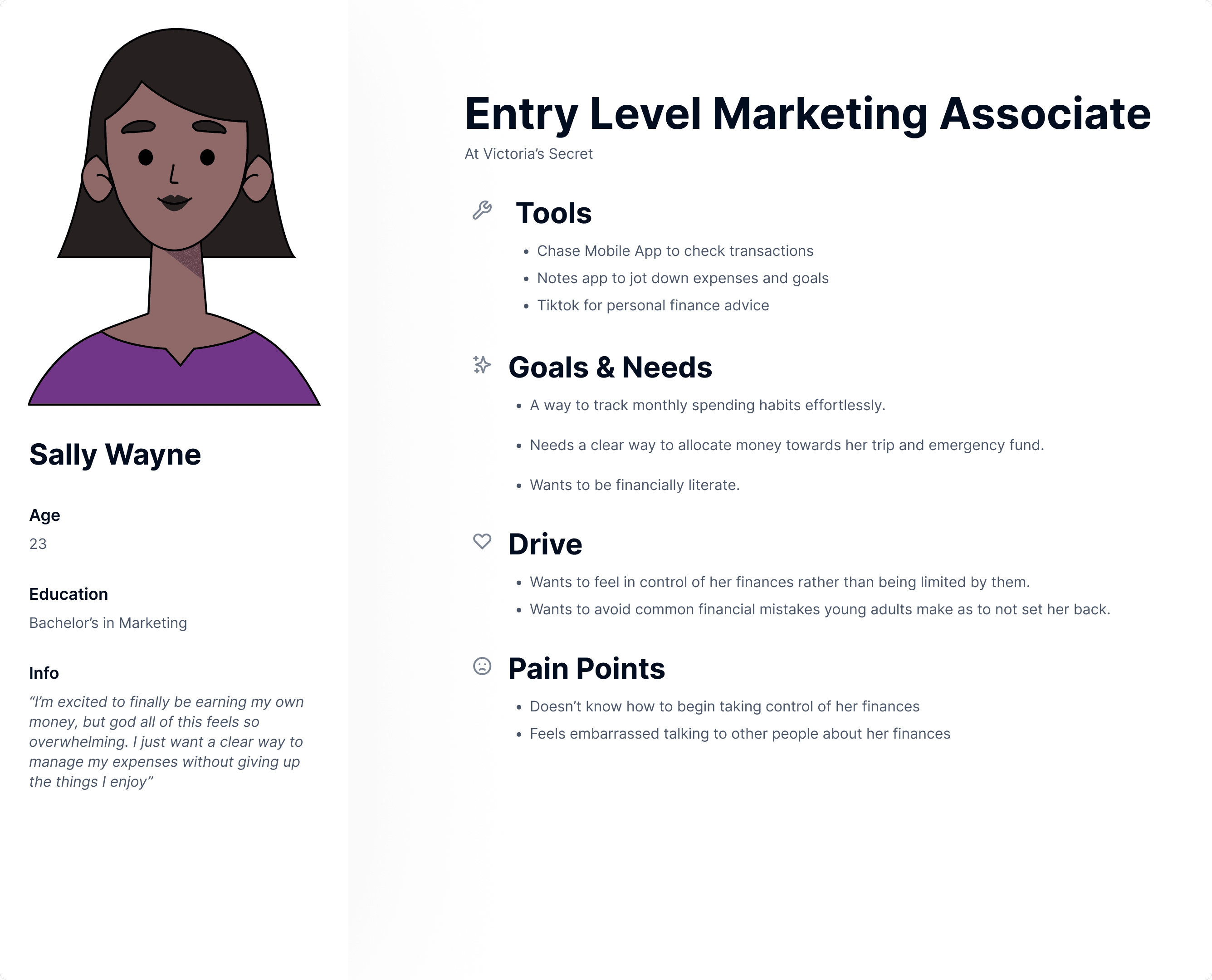

Defining Personas

I created two personas to represent Cashly’s target audience, each embodying key user challenges. Michael Rodgers represents older users navigating the complexities of their finances, while Sally Wayne reflects younger users looking to build strong financial habits early on. These personas serve as a reference point, guiding my design decisions whenever I encounter challenges.

Design

Designing a Simple and Manageable Financial Experience

I designed the main flow with a settled user in mind, due to the platform's viability whether or not a user adds their card for automation. Each key feature/page of Cashly should be isolated from each other so users can approach their finances at a pace that feels comfortable for them.

I adhered closely to a set of product constraints that helped me narrow my focus on the core experience Cashly can provide:

CASHLY IS

For educating users on fundamental financial habits

Meant to be a medium time commitment

Meant to reduce financial anxiety by organizing your finances/assisting you in organizing your finances.

CASHLY IS NOT

A get-rich-quick tool

An investment platform

A set it up and forget about it platform

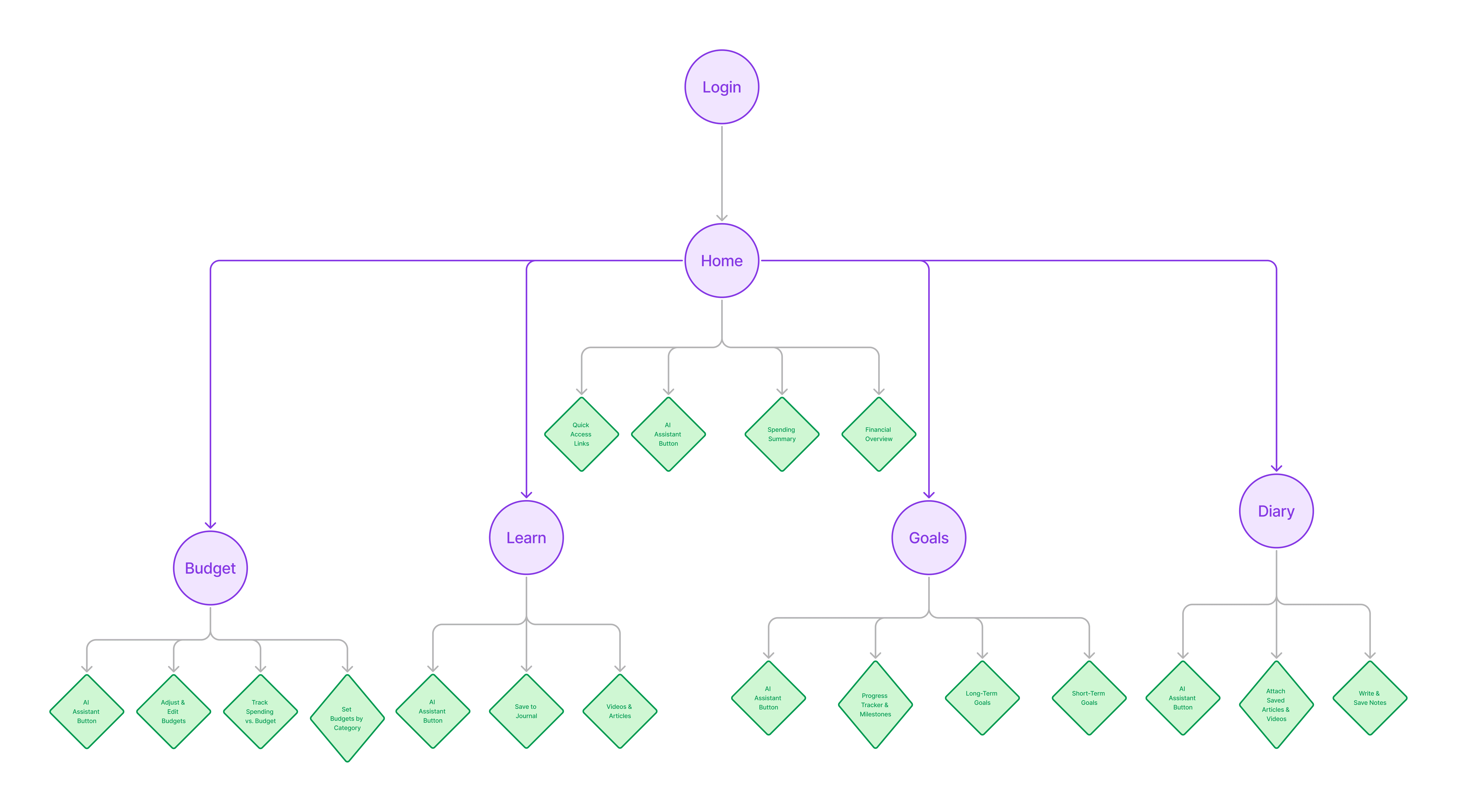

A simple user journey map that reflects everything a user can do and where each action is located

Notable Explorations in Design

Product and design decisions are reflected on every screen of an interface. However, not everything always goes as planned — something I encountered while designing Cashly.

What went wrong?

Users felt too crammed and overwhelmed with mobile designs

"I feel like I'm constantly switching between screens just to find simple information. It's a little frustrating — I wish I could just see everything at once"

"Setting a savings goal took a lot of tapping back and forth. It'd be easier if I had a bigger screen to work with"

Users expressed desire for multitasking

"..when I'm working on my budget, I'd like to have my bank site open too. It's just easier to manage everything on my laptop"

"Every time I had to look at something else, it just makes me think this isn't something I'd like to do on the go"

What I Learned

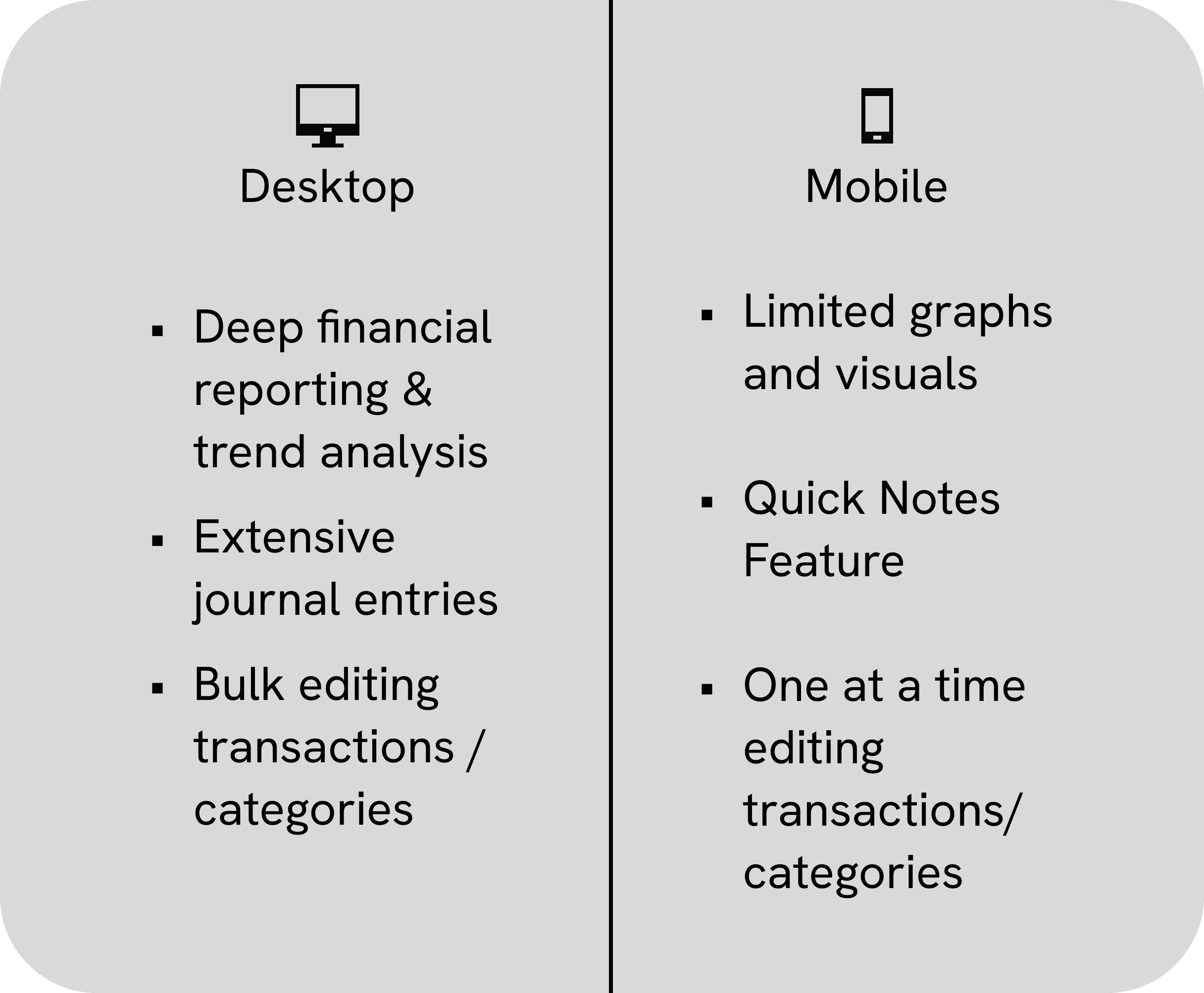

Starting with a mobile-first approach aligned with the initial vision of making Cashly easy and accessible for everyone. However, as the platform grew to support deeper financial planning tools, user feedback made it clear: the small screen limited both functionality and comfort.

I learned that serious financial management often happens when users are sitting down, focused, and multitasking across different tools — behaviors better supported by a web-first experience.

Adapting the Experience

To ensure Cashly fulfilled the original goals outlined in the user flow, I prioritized building out the full functionality on the web platform first. Revisiting user conversations helped me distinguish which actions were best suited for quick, on-the-go tasks versus those that required more attention.

Exploring Color

Originally, Cashly had the following color style picked out: light purple and black. Light purple conveys calm, creativity, and support—ideal for helping users feel at ease while managing financial stress—while also standing out in a crowded fintech space. Black adds clarity, strength, and professionalism, grounding the design and ensuring trust and readability. Together, light purple and black create a modern, balanced visual identity that feels both empathetic and dependable—perfect for guiding users toward financial confidence.

"Since this is basically my financial diary, I think it'd be nice if there was some way to customize the page to make it more 'me'"

Survey questions revolved around four core aspects that would be used to organize the user research through affinity mapping: Pain Points, Direct Wants, Motivation, and Current Tools.

Of the 36 survey respondents, I conducted in-depth interviews with 14 to better understand their financial management experiences. I then organized their insights into an affinity diagram, serving as a key reference point for feature development and design decisions.

Pain points were given roman numerals to identify how many of the interviewees had a specific pain point they ran into.

Key Insights from Research

Users struggle with:

Fragmented financial tool usage

Limited financial literacy

Emotional barriers

Users rely on multiple apps (Acorns for investing, Mint for tracking expenses, YNAB for budgeting) to manage different aspects of their finances. This fragmentation creates friction, as no single tool effectively consolidates all their needs in one place.

Many users experience stress, anxiety, and avoidance when it comes to managing their finances. The fear of seeing low balances, difficulty maintaining financial habits, and feeling like budgeting tools demand perfection contribute to disengagement.

Users struggle with basic financial concepts, such as balancing income with expenses and setting sustainable financial goals. Existing tools assume a level of knowledge users don’t always have, and few provide educational resources to help them develop healthy money habits.

From all of this research, I came to the conclusion that

Financial management is fragmented, overwhelming, and inaccessible—users juggle multiple tools, struggle with anxiety around money, and lack the guidance needed to build lasting financial habits.

This led to me implementing two high-level objectives that guided my design of Cashly

Make financial management simple and time-efficient

Encourage healthy financial habits through actionable steps

Defining Personas

I created two personas to represent Cashly’s target audience, each embodying key user challenges. Michael Rodgers represents older users navigating the complexities of their finances, while Sally Wayne reflects younger users looking to build strong financial habits early on. These personas serve as a reference point, guiding my design decisions whenever I encounter challenges.